When India’s semiconductor ambitions are discussed, attention almost inevitably shifts to fabs and questions around who is building them, where they are located, and whose technology is being used. But during his interview with BW Businessworld, Dr Sandeep Kumar, Chief Executive of L&T Semiconductor Technologies, made a deliberate effort to reframe that narrative.

Sitting in his ninth-floor office at one of the towers inside L&T Tech Park in Bengaluru, Kumar speaks with the calm certainty of someone who has chosen a longer road. “We are a 100 per cent product-focused, R&D-led company today,” Kumar said. “There is no other priority right now.”

That single statement cuts against the grain of current India’s semiconductor discourse. At a time when the country is racing to secure manufacturing capacity, L&T Semiconductor Technologies, which is backed by engineering giant Larsen & Toubro (L&T), has chosen a quieter, longer, and far more capital-intensive path: building semiconductor products from the ground up.

It is a realistic bet rooted in numbers and facts, not nationalism. According to him, L&T Semiconductor’s current R&D spending exceeds the entire outlay of the government’s DLI 1.0 scheme (Rs 1,000 crore or USD 120 million approx.) and all venture capital invested in India’s semiconductor startups combined (about USD 100 million). In effect, the company has emerged as India’s single largest investor in semiconductor product R&D, a distinction that places it in rare company even by global standards. And the company is still in its early days, having been established just two and a half years ago in 2023.

Part of the Industry That Actually Makes Money

The global semiconductor industry is approaching a trillion dollars in annual revenue. But only a fraction of that, roughly USD 250 billion, comes from fabs. The rest flows from products: chips designed for power systems, vehicles, data centres, industrial automation and communications infrastructure.

“That USD 650 billion product market is where value is created,” Kumar says. “Manufacturing matters, but it’s not where differentiation starts.”

This explains why L&T Semiconductor was conceived as a fabless company first, with fab ambitions reserved for later.

Fabless chipmakers have emerged as the dominant engines of value creation in the global semiconductor industry. According to Ken Research, the segment delivered an exceptional 69% compound annual growth in total shareholder returns over five years through 2025, far outstripping every other category in the chip sector

In the global semiconductor ecosystem, this approach aligns more closely with companies that define standards than those that merely supply capacity. It is also an approach that demands patience. Both financial and institutional.

“Semiconductors don’t work on startup timelines,” Kumar says. “You can’t will them into existence.”

The Long Arc of Revenue

In an era shaped by software, investors have grown accustomed to rapid scaling and near-instant monetisation. Semiconductors, however, Kumar points out, operate on a different clock altogether.

“A three-to-four-year sales cycle is normal,” he says. “You design a chip, the customer integrates it into a system, validates it over time, and only then does volume production begin.”

This reality explains why L&T Semiconductor’s revenues are only now beginning to show traction, even as R&D spending has remained elevated. Strategic acquisitions have helped compress timelines by bringing in existing platforms and customer relationships, but they have not eliminated the fundamental physics or economics of the business.

“There are no shortcuts in this business,” Kumar says. “This is a long game.”

That long game also demands restraint in storytelling. While India’s semiconductor push has often been accompanied by optimistic projections, Kumar is careful not to overstate what lies ahead. “Any growth curve you draw today is still a projection,” he says. “We’re still early.”

Why SiC and GaN Matter More Than Silicon

If L&T Semiconductor’s strategy has a technological centre of gravity, it seemingly lies in wide-bandgap semiconductors, specifically Silicon Carbide (SiC) and Gallium Nitride (GaN).

These materials are transforming how power is managed and consumed. They allow systems to operate at higher voltages, temperatures and frequencies, reducing energy loss and physical footprint.

“This isn’t about a marginal improvement,” Kumar says. “It’s about system-level transformation.”

Source: Mordor Intelligence Source: Mordor Intelligence

In electric vehicles, SiC can extend driving range. In data centres, GaN can reduce cooling requirements. In power grids, both can improve efficiency at scale. As economies electrify and decarbonise, these gains compound.

“This is not niche,” Kumar says. “Energy, power, EVs, data centres. This is where the world is headed.”

Over time, Kumar expects these technologies to become L&T Semiconductor’s largest revenue engine, even if industrial and communications products generate earlier cash flows.

Demand Does Not Equal Victory

One of Kumar’s sharpest critiques is reserved for the idea that India’s electronics market will naturally favour Indian chipmakers.

“India demand does not mean India design wins,” he says.

Semiconductor sourcing decisions, he explains, are global by default. Performance, reliability, cost and long-term supply assurance matter far more than geography. To make the point, Kumar references Apple.

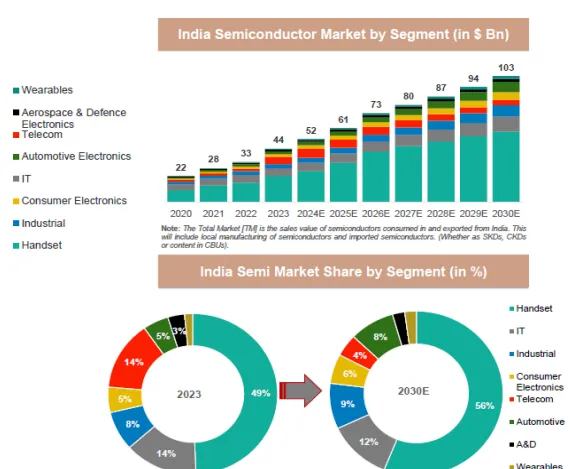

Source: India Semiconductor Market Report by IESA Source: India Semiconductor Market Report by IESA

“Apple doesn’t choose chips because of where they’re made,” he says. “They choose the best chip for the product.”

With hundreds of chips inside a single smartphone or any vehicle, the notion of wholesale import substitution collapses under its own complexity. “No company replaces everything,” Kumar says. “You win specific sockets. That’s how this industry works.”

For Indian firms, that means competing globally from day one and not relying on domestic preference, contrary to the rhetoric playing out widely in the country.

Europe, Neither India nor US, the First Big Market

While L&T Semiconductor is headquartered in India, its early growth is being driven elsewhere. Europe, in particular, has emerged as a critical market.

The reasons are structural. Europe’s aggressive push into electric mobility, renewable energy and industrial electrification works well for L&T Semiconductor’s product portfolio. Add to that the continent’s desire to diversify supply chains away from China, and the opportunity becomes clear.

“Europe is moving faster than most regions on energy transition,” Kumar says. “That creates demand now, not later.”

Here, the broader L&T brand also provides an edge, he says. In industries where product lifecycles span decades, trust is currency. “Customers want to know their supplier will be around,” Kumar says. “That matters.”

India and Japan, too, contribute early revenues, but Europe is expected to dominate growth in the near to medium term, Kumar adds.

Fabs First Was Optics but Necessary for India

When asked if India going with manufacturing semiconductor was the right move despite having the design talent and prowess, Kumar does not dismiss India’s fab-first policy approach. In fact, he defends it, but up to a point.

“You needed something big and visible,” he says. “Fabs signal seriousness to the world.”

In a geopolitical moment shaped by supply-chain fragility, fabs offered clarity and credibility. But Kumar is clear-eyed about what must come next.

“Without design funding, momentum breaks,” he says.

Design, unlike manufacturing, does not benefit from one-time announcements. It requires institutional, repeatable capital. To that end, Kumar advocates a US-style SBIR (Small Business Innovation Research) and Small Business Technology Transfer (STTR) programmes, where ministries are mandated to allocate a portion of their budgets to innovation and problem-led R&D.

“That creates continuity,” he says. “And continuity is what the design ecosystem needs in India.”

Still Building, Still Early

Despite its scale and ambition, L&T Semiconductor remains a work in progress. Kumar places the company two years into a five-to-seven-year journey, with profitability and public markets still distant milestones.

He has said previously that the company would want to cross USD 500 million in annual revenue before even considering a public listing, and would only begin evaluating the case for a fabrication facility after reaching a USD 1 billion annual revenue run rate.

“This is foundational work,” he says. “It takes time.”

In an ecosystem often dominated by immediate wins and headline numbers, L&T Semiconductor’s approach stands apart. It is slower, heavier, and less visible, but potentially more enduring.

As India seeks its place in the global semiconductor order, Kumar’s argument is simple: fabs may open doors, but products decide who stays in the room. And for L&T Semiconductor, that work seems to have only begun. |